Supply and demand relationship restored, and prices rose month-on-month in 1st Quarter of 2025.

【Introduction】 Although affected by factors such as the Spring Festival holiday and the downward trend of international oil prices, the supply and demand relationship of the domestic maleic anhydride market in the first quarter of 2025 has been significantly repaired, and the price center of gravity has risen month-on-month. In the second quarter, due to the strong expectation of increased production on the supply side, the process of repairing the supply and demand relationship may come to a temporary end, and the price of maleic anhydride will continue to be under pressure.

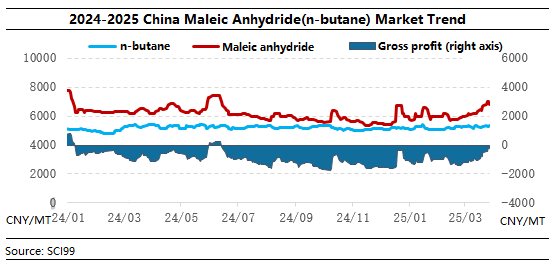

In the first quarter of 2025, the domestic maleic anhydride market was overall strong and volatile. The average price of the major domestic markets in the first quarter was 6,598 CNY/ton, up 5.42% month-on-month and down 4.29% year-on-year. In January and February, the downstream demand for maleic anhydride was at a low level throughout the year due to the Spring Festival holiday. The market situation mainly revolved around the changes in the start-up of the supply-side equipment, and the price trend was relatively volatile. After entering March, the supply and demand of maleic anhydride recovered faster. The supply and demand relationship was in a tight state for a long time due to the relatively rapid growth in demand, which prompted the maleic anhydride price to increase rapidly since mid-month, but the scale of the resumption of production plan for the previous maintenance equipment increased again near the end of the month, and the production increase trend caused the price to begin to fall from a high level. Taking the price of liquid anhydride in Shandong market as an example, the high point of maleic anhydride price in the first quarter was 7,000 CNY/ton on March 24, and the low point was 5,700 CNY/ton on January 2, with a price difference of 1,300 CNY/ton.

The decline in supply is relatively large, and the contradiction between supply and demand has eased marginally.

Although the performance on the demand side is relatively general, under the background of contraction on the supply side, the contradiction between supply and demand in the maleic anhydride market in the first quarter has eased compared with the fourth quarter of 2024, providing strong upward momentum for prices. In terms of supply, from January to March, only 210,000 tons/year of Hengli Petrochemical’s production capacity was added in China, and the supply capacity has not been fully released. The remaining maleic anhydride stocks also ushered in the peak period of maintenance before and after the Spring Festival, and there were also many plant shutdowns and load reductions. This led to a 5.04 percentage point month-on-month decrease in the operating load rate of domestic maleic anhydride plants in the first quarter, and a 7.29% month-on-month decrease in output. In terms of demand, although domestic demand was at the “bottom” level of the whole year before and after the Spring Festival holiday, the downstream unsaturated resin industry started work quickly after mid-February and recovered to a normal level of around 34%. Maleic anhydride exports also continued to maintain growth momentum. The total consumption in the first quarter only decreased by 4.96% month-on-month, which was 2.33 percentage points lower than the decline in supply. Therefore, the contradiction between supply and demand of domestic maleic anhydride products will be effectively repaired in the first quarter of 2025, which will boost the market conditions.

Raw material costs remain high, weak oil price interference is effective

In the first quarter, the raw material n-butane maintained high fluctuations, and there was a strong bottom support for maleic anhydride prices. Although the international oil price trend was weak in the first quarter, and there was a lack of favorable guidance for related products, the raw material n-butane market was strong under the support of local supply tightening and downstream rigid demand. The average price in the first quarter still rose by 2.45% month-on-month, pushing the average cost of n-butane-based maleic anhydride to rise by 1.92% month-on-month, providing strong support for maleic anhydride prices. Due to the relatively large increase in maleic anhydride prices, the average gross profit of n-butane-based maleic anhydride in the first quarter also rose by 21.06% month-on-month, especially the rapid rise in the market after mid-March, which once brought the maleic anhydride gross profit close to turning losses into profits. However, the improvement in profitability also stimulated the production enthusiasm of maleic anhydride companies, and the pressure of increasing supply also caused prices to fall back.

The contradiction between supply and demand may worsen again in the second quarter, and the market may be mainly weak and volatile

Looking forward to the second quarter, the raw material n-butane may maintain high volatility, and the cost side will still support the price of maleic anhydride. However, there are many new production capacity commissioning and stock plant resumption plans on the supply side, and the strong supply and weak demand pattern may be strengthened again, which will form a long-term suppression on the market trend, especially increasing the difficulty of upward breakthrough. It is expected that the domestic maleic anhydride market as a whole will maintain a weak and volatile operation trend in the second quarter, and the industry as a whole is still in the capacity digestion cycle.