In the past month and a half, maleic anhydride has experienced two waves of rising prices. The market activity has increased significantly, and the frequency of price fluctuations has also increased significantly. The main driving factor causing price fluctuations is still the performance of the supply side. The expected commodity volume and the actual commodity volume are different. There is a discrepancy between the quantity and the fulfillment situation, and the supply and demand game has ordered the supplier to regain the pricing power, and the market has opportunities for growth.

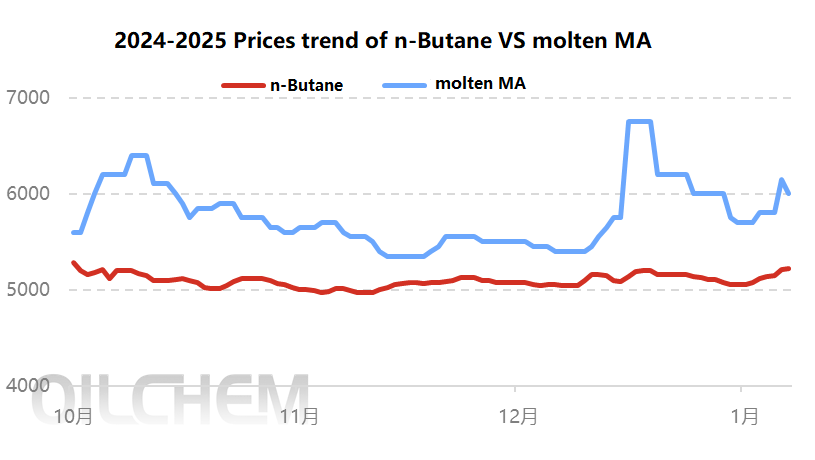

As shown in Figure 1, maleic anhydride has shown a clear downward trend since the fourth quarter of 2024, and continued to hover at a low price in November, with a lack of driving factors for prices. The shrinking profits of the main downstream maleic anhydride and the increasing cost pressure have also constrained the price operation of n-butane. The price operation range in the second half of the year is significantly lower than that in the first half of the year. Since the fourth quarter, the high point of n-butane has been around 5,200 yuan/ton, and the price difference between n-butane and molten (liquid) maleic anhydride has narrowed to less than 300 yuan, which has brought great resistance to the production and operation of maleic anhydride enterprises. At the end of November, Shandong’s large factories once again reduced their operations and the volume of goods decreased. This also provided an opportunity for the maleic anhydride market to rise by thousands of yuan per day in mid-December due to the unexpected shutdown of the production in Yantai. Entering January, the variable volume of molten (liquid) maleic anhydride goods brought a second opportunity for maleic anhydride to rise.

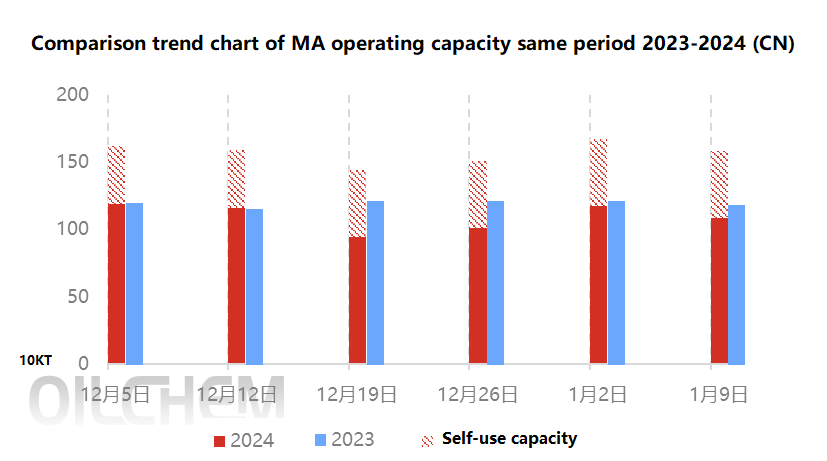

Since 2024, the growth rate of supply has been significantly higher than the growth rate of demand. Why did the supply market regain pricing power in December? As shown in Figure 2, although the operating capacity of maleic anhydride in December 2024 was around 1.5-1.7 million tons, Hengli did not release the volume of liquid anhydride to the market since December, and most of the liquid anhydride was used for self-use. Therefore, excluding the part used by Hengli, the operating capacity of maleic anhydride in December was around 1-1.2 million tons; compared with the same period in 2023, the operating capacity of maleic anhydride in December 2023 was around 1.1-1.2 million tons, which was slightly higher than the level in 2024. Therefore, maleic anhydride showed a slightly tight supply in December, and the supply and demand were relatively balanced. This is also one of the main factors that enable the supplier to regain the initiative.

Positive factors:

Negative factors:

(Source: Oilchem)