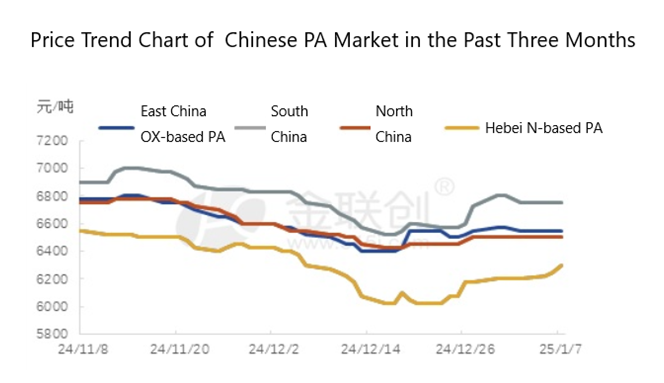

At the beginning of 2025, driven by the high operating rate and high demand from the downstream in the domestic phthalic anhydride market, the spot inventory has become tight. Coupled with the continuous losses in the PA industry, the willingness of industry players to support prices has strengthened, driving the overall focus of the market to rise. As of January 20th, the negotiated price of OX-based PA in the East China region was referred to as 7200 yuan/ton for self-pickup, and the price of N-based PA in the northern region was referred to as 6900 yuan/ton for self-pickup.

After the New Year’s Day holiday, the international crude oil price showed a relatively strong upward trend, and the news was generally favorable. The market for the upstream raw material o-xylene remained stable, and the industrial naphthalene market strengthened and rose. These factors provided relatively strong support for the cost side of PA. In the o-xylene-based PA industry, under the situation of long-term upside-down profits, the mentality of industry players to support prices became stronger.

The main reason for the bottoming out and rebound of the PA market starting from late December was the tight supply and demand situation. On the one hand, downstream plasticizer enterprises had sufficient orders, and the operating rates of DOP and DBP both increased to a high level of over 75%. Their output was on the rise, which led to a significant increase in the demand for PA, resulting in a tight supply in the phthalic anhydride market and thus driving up prices. On the other hand, the overall capacity utilization rate of the domestic PA industry did not increase significantly. The operation of OX-based phthalic anhydride was stable, and the operation of the N-based PA industry had a slight increase. Recently, with the restart and resumption of the PA units of Kailuan in Tangshan, Baogang in Zhanjiang and Sanmu in Henan, the overall operating rate of PA increased to over 65%. However, in the face of the strong demand from the downstream, over-selling was common among PA enterprises. Some of the N-based PA sources in the northern region were even oversold until mid to late January. Therefore, the mentality of PA industry players to support prices was strong, which promoted the gradual rise of the focus of the PA market.

Looking ahead, until before the Spring Festival, the PA market will probably continue to maintain a trend of price support and fluctuations. Currently, the tight situation of spot supply in the domestic PA industry may still be difficult to ease. The main downstream plasticizer industry is operating at a high level, and some enterprises are restocking in advance before the Spring Festival holiday. In the short term, the trading atmosphere in the market may remain good, and industry players are active in their operations. Manufacturers may take advantage of the situation to push up the shipment prices.

However, as the Spring Festival approaches, the operating rate of the plasticizer industry is expected to decline. The demand from other downstream industries such as UPR is also weakening. By then, the market restocking will basically come to an end. Downstream enterprises will successively shut down for the holiday, and the market demand will slow down. As a result, the PA market may enter a transitional stage of sideways consolidation.

(Source: JLC)