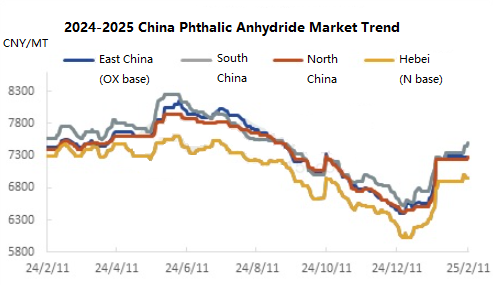

Introduction: Following the Spring Festival holiday, the domestic phthalic anhydride market has seen a slight upward adjustment in prices. Holders of the product are optimistic about the post-holiday market, and some manufacturers have a strong inclination to push prices up due to oversold inventories, leading to a slight increase in the focus of negotiations. As of the close on February 11th, the reference price for ortho-phthalic anhydride in East China is 7300-7350 yuan/ton ex-works, while the price for naphthalene-based phthalic anhydride in the north is around 6950-7000 yuan/ton ex-works, both showing an increase of approximately 50-100 yuan/ton compared to pre-holiday levels.

On the cost side, the continuous rise in raw material prices has provided strong support. On Monday (February 10), Sinopec’s listed price for ortho-xylene increased slightly by 100 yuan/ton to 7300 yuan/ton, bringing the raw material price almost on par with the price of phthalic anhydride. The strong price of ortho-xylene has directly raised the production cost of ortho-phthalic anhydride, while the price of industrial naphthalene has also shown a strong consolidation trend. The cost linkage between the two types of phthalic anhydride has jointly pushed up the overall market focus.

The tight supply situation continues. During the Spring Festival holiday, the shutdown of some units further reduced supply, with manufacturers’ inventories at low levels. Most companies are still focused on delivering previous orders. After the holiday, the operating rate of domestic phthalic anhydride units remained at 60%-65%, and the slow recovery of capacity utilization in the initial post-holiday period has led to tight spot circulation. Recently, the situation for phthalic anhydride export orders has been favorable, which has also helped alleviate domestic inventory pressure. The role of phthalic anhydride exports in regulating domestic supply and demand balance remains significant.

On the demand side, post-holiday restocking expectations are evident. The operating rate in the plasticizer industry has rebounded, with DOP and other plasticizer companies gradually resuming production after the Spring Festival. The operating rate has recovered from the holiday lows, providing some short-term pull on phthalic anhydride. Although the demand for unsaturated resin is recovering slowly, the expected improvement in demand from infrastructure, real estate, and other sectors after the holiday will provide a floor for the phthalic anhydride market in the medium to long term.

In terms of future market predictions, after Sinopec’s push to raise ortho-xylene prices, there is some support for the ortho-phthalic anhydride industry. Another raw material, industrial naphthalene, may also see an upward trend. In the short term, the domestic phthalic anhydride market, supported by cost and restocking demand, may continue to show a firm price trend. However, terminal demand has not fully recovered, and downstream sectors are still consuming previous inventories, with limited new orders. It is necessary to monitor the sustainability of downstream procurement and the impact of international crude oil price fluctuations on the raw material ortho-xylene.

(Source: JLC)