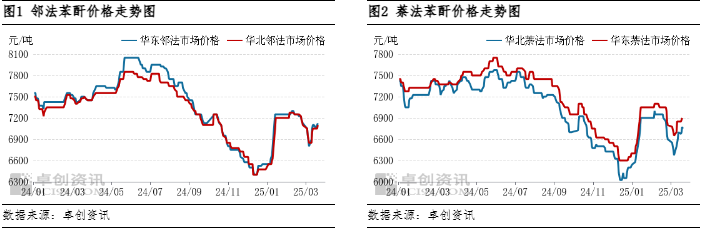

During this period, the center of gravity of the o-method and naphthalene-method phthalic anhydride market prices moved up slightly, and the weekly average price rose. The weekly average price of o-method phthalic anhydride in East China was 7085 yuan/ton, up 95 yuan/ton from the weekly average price last week, an increase of 1.36%; the weekly average price of naphthalene-method phthalic anhydride in North China was 6720 yuan/ton, up 175 yuan/ton from the weekly average price last week, an increase of 2.67%.

Main factors affecting the price trend of phthalic anhydride market in this cycle: On the cost side, the raw material o-xylene market operated steadily, the price of industrial naphthalene market continued to rise, and the cost support increased; on the supply side, some phthalic anhydride units such as Tangshan Kailuan and Nanjing Libang were shut down, and the overall supply decreased; on the demand side, the main downstream market was still flat, the willingness to enter the market to purchase was insufficient, and most of the inquiries were rigid demand. Comprehensive analysis shows that the cost support of the phthalic anhydride market this week is still strong, the supply is reduced, the demand is stable, and the focus of market negotiations has moved up compared with last week.

Crude oil: This week, the overall oil price showed a narrow range of fluctuations, and the fluctuation range of US crude oil was between 66 and 68 US dollars per barrel. This week, the average price of US crude oil was 67.07 US dollars per barrel, an increase of 0.4 US dollars per barrel, or 0.6% from last week; the average price of Brent crude oil was 70.57 US dollars per barrel, an increase of 0.65 US dollars per barrel, or 0.93% from last week. In response to the Ukrainian issue, the United States and a European country negotiated. From the released news, the negotiations progressed well, and it was initially determined to abandon the plan to attack the other party’s energy facilities in order to promote the peace process and continue to cool down the oil market; however, the Middle East issue was in turmoil again, Israel launched a new attack, and the Houthi armed forces also clashed with the United States near the Red Sea, and the Middle East geopolitical issues re-emerged; the Federal Reserve suspended interest rate cuts and maintained the interest rate level unchanged, which was in line with market expectations; US oil inventories had limited guidance on the current crude oil price, which was basically in line with seasonal laws. Therefore, the geopolitical risks in the oil market are still repeated, and the macro and fundamentals are also in line with expectations, and oil prices are mainly in a narrow range of fluctuations.

Raw material o-phthalate: The o-xylene market has been running strong during this period. As of the close of March 20, the o-xylene market price in East China was 7,500 yuan/ton, which was the same as the previous closing price. Market news said that a set of equipment of Yangzi Petrochemical began maintenance on the 17th, and the market volume decreased significantly. In addition, the foreign market price is still high, and the price difference between the domestic and foreign markets still exists, so the market support is still relatively strong. The operating load of downstream o-phthalic anhydride has dropped slightly, and the demand for o-xylene has weakened, but the impact is not significant. The market atmosphere of raw material xylene is stalemate, and the cost support is also limited. At present, the o-xylene market is mainly supported by the shortage of supply and is running steadily as a whole.

Raw material industrial naphthalene: The domestic industrial naphthalene market fell narrowly this week. As of the close of Thursday this week, the mainstream transaction price in the Shandong market was 5,150-5,150 yuan/ton, and the high-end price fell by 50 yuan/ton last Thursday. The main reasons for the changes in market prices this week are: 1. The operating load of naphthalene-based phthalic anhydride enterprises in the downstream main consumption field has decreased, and the manufacturers have weakened their purchasing power for industrial naphthalene on the raw material side, the bargaining sentiment is strong, and the demand for industrial naphthalene has decreased. 2. The operating load of deep processing enterprises has increased slightly, and the overall supply of industrial naphthalene has increased slightly, but the inventory pressure of manufacturers is not large, and the willingness to support prices is strong. 3. The center of gravity of the high-temperature coal tar market on the raw material side has moved downward, and the cost side of industrial naphthalene has lost support. Overall, the industrial naphthalene market has peaked and fallen, but the decline is limited.

From the perspective of cost, the market price of raw material o-xylene is stable, and the market price of industrial naphthalene first rose and then fluctuated narrowly. The cost side support still exists, and coupled with the decline in phthalic anhydride supply, the center of gravity of the market price has moved up narrowly.