Chinese domestic Phthalic Anhydride Weekly Review: Cost support strengthened, supply decreased, and the market rebounded

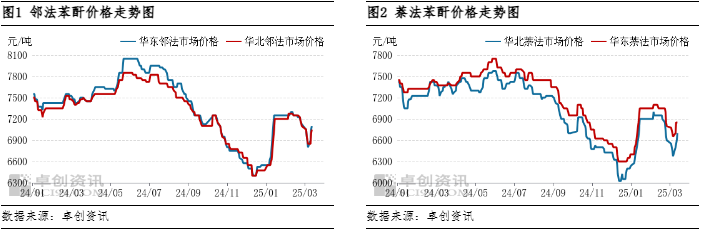

During this period, the market prices of ortho-method and naphthalene-method phthalic anhydride rebounded. The average weekly price of ortho-method phthalic anhydride in East China was 6,990 yuan/ton, up 30 yuan/ton from the average weekly price last week, an increase of 0.43%; the average weekly price of naphthalene-method phthalic anhydride in North China was 6,545 yuan/ton, up 40 yuan/ton from the average weekly price last week, an increase of 0.61%.

The main factors affecting the price trend of phthalic anhydride market in this cycle: On the cost side, the raw material o-xylene and industrial naphthalene units fluctuated, supply decreased, among which the market price of industrial naphthalene increased, and the cost side support increased; on the supply side, some phthalic anhydride units such as Tangshan Xuyang, Tangshan Huayi, Hubei Nengtai, etc. were shut down, and supply decreased; on the demand side, the main downstream was affected by the upward trend, and rigid demand purchases followed up, but the sustainability was limited. Comprehensive analysis shows that this week the cost side support of the phthalic anhydride market increased, supply decreased, trading atmosphere rebounded, and the price center of gravity moved up.

Crude oil: This week, the overall oil price showed a low-level fluctuation, and the fluctuation range of US crude oil was between 66 and 68 US dollars per barrel. This week, the average price of US crude oil was 66.67 US dollars per barrel, down 1.94 US dollars per barrel, or 2.82% from last week; the average price of Brent crude oil was 69.92 US dollars per barrel, down 1.91 US dollars per barrel, or 2.66% from last week. The low-level fluctuation of oil prices, although there are signs of stabilization, is still weak. Even if it rebounds, the strength is average and the continuity is not strong. The main negative factor comes from the US trade war. In addition to the previous mutual increase and escalation of tariffs with China, tariffs with Canada, Mexico and other countries are also being increased, and tariffs on steel and other areas and countries are also being promoted. Against the background of the trade war, the US stock market has ushered in a continuous decline, dragging down the crude oil market. However, the announced reduction in US gasoline inventories is large, which partially corrects the pessimistic expectations of weakening demand in the previous period. After the low-level fluctuation, the oil price rebounded moderately, but it was generally in a low-level narrow consolidation market.

Raw material o-phthalate: The o-xylene market has been running strong during this cycle. As of the close of March 13, the o-xylene market price in East China was 7,500 yuan/ton, which was the same as the closing price of the previous period. Last Friday, market news said that a set of equipment of Yangzi Petrochemical had failed and it was planned to start maintenance in the second half of the month. The market volume has decreased significantly. In addition, the foreign market price is still high, and the price difference between the domestic and foreign markets still exists, so the market support is still relatively strong. The operating load of downstream o-phthalic anhydride has dropped slightly, and the demand for o-xylene has weakened, but the impact is not significant. The trend of raw material xylene has weakened, and the support on the cost side has loosened, but the o-xylene market is currently supported by the shortage of supply, and the market is running steadily.

Raw material industrial naphthalene: The domestic industrial naphthalene market has been rising this week. As of the close of Thursday this week, the mainstream transaction price in the Shandong market was 5,200-5,200 yuan/ton, and the high-end price rose by 400 yuan/ton last Thursday. The main reasons for the market price changes this week are: 1. The center of gravity of the naphthalene-based phthalic anhydride market in the downstream main consumption field has moved up, and manufacturers have increased their purchase of industrial naphthalene on the raw material side, and the demand for industrial naphthalene has increased. 2. The operating load of deep processing enterprises has decreased, the overall supply of industrial naphthalene has decreased, and the overall supply and demand are tight. Overall, the center of gravity of the industrial naphthalene market has moved up.

From the perspective of cost, the market price of raw material o-xylene is stable, the market price of industrial naphthalene has rebounded, the cost side support has been strengthened, and the downstream demand for phthalic anhydride is still acceptable, and the market price has stopped falling and rebounded narrowly.

Crude oil: Next week, oil prices are expected to continue to fluctuate, with an average price of US crude oil of US$68 per barrel and a fluctuation range of US$65-70 per barrel. After the negotiations between the United States and Ukraine, Ukraine basically agreed to suspend the 30-day ceasefire agreement, but whether a certain European country will end it is still uncertain and needs to be continuously monitored. In addition, after the three major monthly reports are released one after another, the market may give strong support to oil prices for the issue of oil export restrictions on a certain Middle Eastern country, and the possibility of negotiations between the United States and Iran in the short term is low. Therefore, the market news is a long-short game, and oil prices are likely to maintain the current position and continue to fluctuate. From the perspective of risks, one is the destocking of US crude oil; the other is the disturbance of the European situation.

Raw material o-phthalate: The operating load of the main downstream o-phthalic anhydride is expected to decline, and the demand for o-xylene will decrease, but with the official start of maintenance by Yangzi Petrochemical, the domestic market supply tension has intensified, and the price of o-xylene in the foreign market is still high, and the o-xylene market may continue to operate steadily. The market price of o-xylene may hover around 7,500 yuan/ton, and the average price may be 7,500 yuan/ton.

Raw material industrial naphthalene: The domestic industrial naphthalene market may see a narrower increase next week. The mainstream transaction price in Shandong is expected to be 5,200-5,250 yuan/ton. In terms of demand, the operating load of the downstream naphthalene-based phthalic anhydride market may increase slightly next week, and the overall demand for industrial naphthalene is expected to increase slightly. However, due to the poor shipment of the downstream naphthalene-based phthalic anhydride market, the price may be expected to fall back, and enterprises are somewhat resistant to the high supply of raw material industrial naphthalene. In terms of supply, the operation of deep processing enterprises has not yet fully recovered, and the supply of industrial naphthalene remains tight. Combining the above factors, it is expected that the industrial naphthalene market will maintain a strong trend next week, but the increase may narrow.

Downstream DOP: There is still a small profit-making action in the raw material octanol market, the phthalic anhydride market is in a consolidation operation, and the cost support of DOP may decline steadily. There is still no obvious improvement in the downstream order situation, and the possibility of further reduction in demand for raw materials remains, which will form a negative pressure on the market. However, under the inventory pressure of major DOP factories, there is still a continued reduction in negative pressure. With the expectation of supply reduction, it is expected that the DOP market price may fall steadily next week, but the decline will not be large.

The domestic phthalic anhydride market will be mainly consolidated next week, and some market prices may be loose at high levels. The market price of ortho-phthalic anhydride in East China may be 7000-7100 yuan/ton, and the weekly average price may be around 7010 yuan/ton. From the cost side, the market price of raw material ortho-xylene remains stable, and the market price of another raw material industrial naphthalene is strong, and the supply of raw materials is tight, so the cost side support still exists; from the supply side, some factories such as Shandong Zhongtai and Hubei Nengtai are running, and some factories such as Taizhou Liancheng, Jiangsu Sanmu, Tangshan Kailuan, etc. are stopped, and the overall supply is slightly reduced; from the demand side, the main downstream market is sluggish, the operating load rate is limited, and most of them maintain rigid demand for goods. Based on the above analysis, the cost support of phthalic anhydride will still exist next week, the supply will drop slightly, the demand will be flat, the market may tend to be consolidated, and the high prices in some local markets may be loosened.