Why are global chemical giants abandoning the MMA market? How will the competitive environment of MMA in China be affected?

Firstly, the global MMA (methyl methacrylate) production capacity is mainly distributed in Asia. As of mid-2024, the global production capacity of MMA (methyl methacrylate) is nearly 6 million tons per year, distributed across Asia, the Americas, Europe and the Middle East. Among them, the production capacity in Asia is nearly 4 million tons per year, accounting for 66% or more of the global total production capacity. Asia is the largest production base and its main consumer market is also in Asia, concentrated in Northeast Asia. As a result, Asia has become the main competitive market for MMA, and the competitive environment has deteriorated. This is one of the main considerations for Kuraray to reduce its MMA production capacity in Asia.

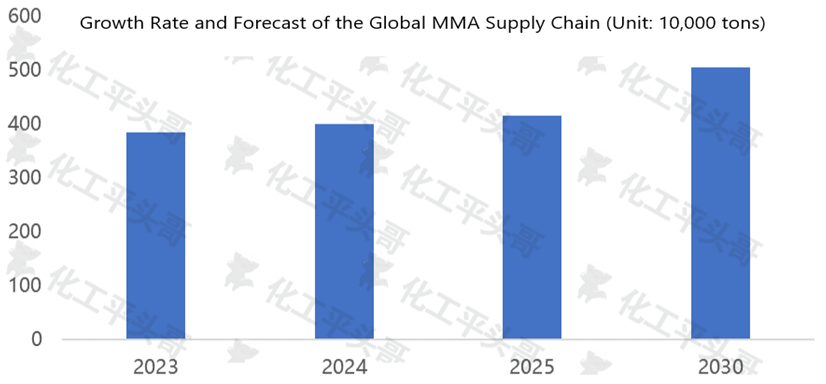

Secondly, the global production capacity has maintained a high growth rate, and the growth in Asia is particularly noticeable.In 2020, Mitsubishi took the lead in abandoning the MMA market in the UK, and Kuraray reduced its competition in the Northeast Asian market. The main reason might be the rapid growth of the global supply side of MMA. By the end of 2023, the global output of MMA was close to 4 million tons per year. It is expected that the global output of MMA will exceed 5 million tons per year by 2030. During the period from 2023 to 2030, the global output of MMA is expected to maintain a growth rate of 4%, which will surely lead to a more severe market competition environment. For international chemical enterprises, predicting the global market and making corresponding decisions is the key to reducing their own competitive risks.

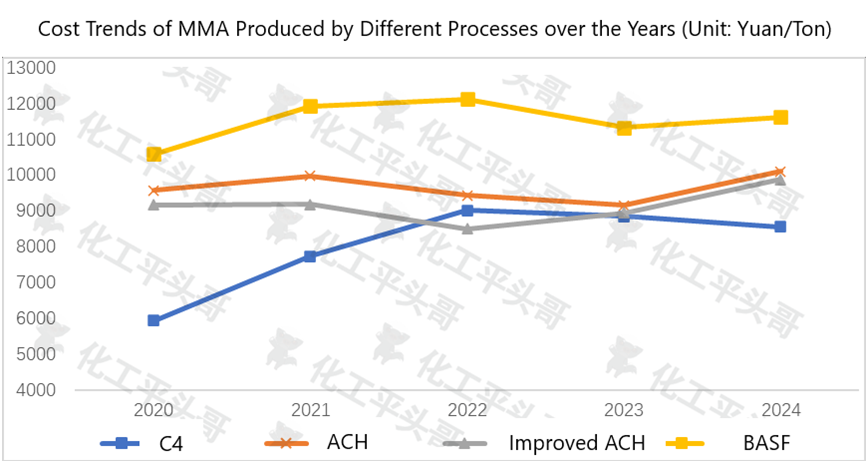

Thirdly, the competition among different processes is obvious, and the profit margins of traditional processes are shrinking.

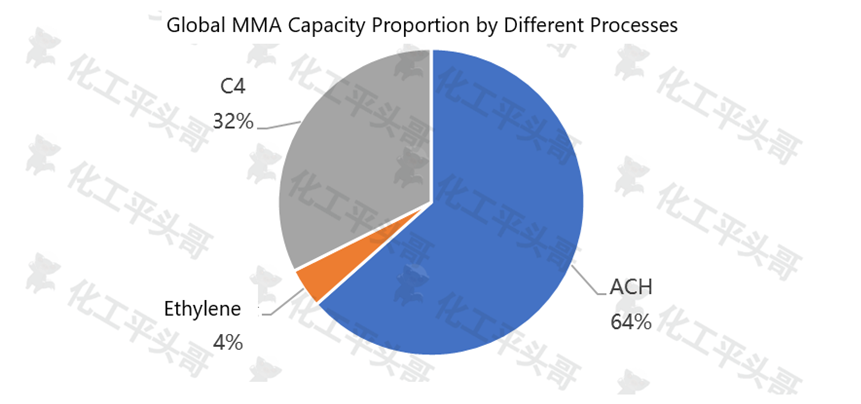

By the end of 2023, in the global MMA production facilities, the production capacity of the ACH process accounted for 64%, making it the most commonly used production method. The C4 process accounted for approximately 32%. It can be seen that the competition in the global MMA production process mainly focuses on the ACH process. The main reason why enterprises mostly choose to adopt the ACH process is that it can be matched with the hydrocyanic acid produced as a by-product of acrylonitrile by themselves, which can reduce production costs to a certain extent.

The following situations can be known from the chart:

1.The competitiveness of MMA produced by the ACH method has been gradually declining in the past few years because of the consistently high cost of acetone.

2.The production capacity of MMA produced by the ACH method accounts for the largest proportion globally. Under the premise of product homogeneity, most of the market competition revolves around costs, which has led some enterprises to be unable to withstand the competitive pressure and choose to withdraw from the market. 3.The cost difference between the C4 method and the ACH method is significant, and the market influence factors on their basic raw materials are obviously different. Affected by the new energy vehicle industry, there is a high probability that MTBE will experience weak fluctuations in the future, which also strengthens the expectation that the cost of C4 will remain at a low level continuously.

Fourthly, the competition from downstream substitutes is becoming increasingly fierce, and the growth rate of PMMA (polymethyl methacrylate) consumption is decreasing.

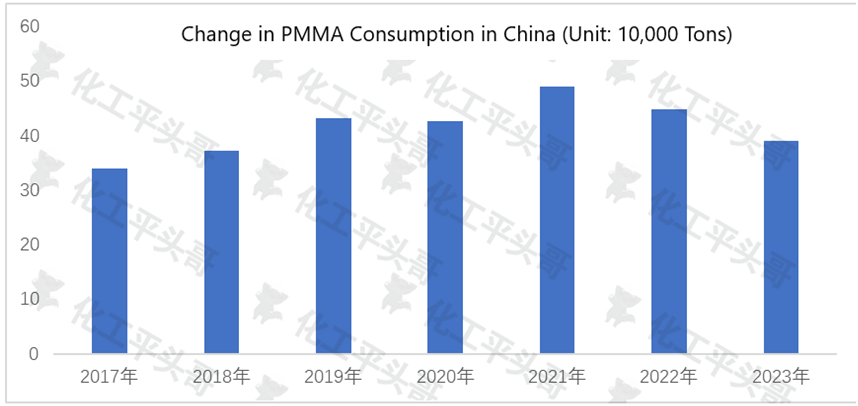

Over 56% of MMA downstream is used for the production of PMMA, which is the largest downstream application area of MMA. According to relevant data, from 2017 to 2023, the average annual growth rate of PMMA consumption in China was only 2.3%. It has been gradually shrinking since 2021 and had dropped to around 380,000 tons by 2023. The reasons for the gradual decline in PMMA consumption are as follows: First, homogeneous products are very serious; second, the competition from substitutes is accelerating.